UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

SCHEDULE 14A

(Rule 14a-101)

INFORMATION REQUIRED IN PROXY STATEMENT

SCHEDULE 14A INFORMATION

Proxy Statement Pursuant to Section 14(a) of the

Securities Exchange Act of 1934.

Filed by the Registrant x

Filed by a Party other than the Registrant ¨

Check the appropriate box:

¨ | Preliminary Proxy Statement |

¨ | Confidential, for Use of the Commission Only (as permitted by Rule 14a-6(e)(2)) |

x | Definitive Proxy Statement |

¨ | Definitive Additional Materials |

¨ | Soliciting Material under Section 240.14a-12 |

CARROLS RESTAURANT GROUP, INC.

(Name of Registrant as Specified in its Charter)

(Name of Person(s) Filing Proxy Statement if other than the Registrant)

Payment of Filing Fee (Check the appropriate box):

x | No fee required. |

¨ | Fee computed on table below per Exchange Act Rules 14a-6(i)(1) and 0-11. |

1) | Title of each class of securities to which transaction applies: |

2) | Aggregate number of securities to which transaction applies: |

3) | Per unit price or other underlying value of transaction computed pursuant to Exchange Act Rule 0-11 (Set forth the amount on which the filing fee is calculated and state how it was determined): |

4) | Proposed maximum aggregate value of transaction: |

5) | Total fee paid: |

¨ Fee paid previously with preliminary materials.

¨ Check box if any part of the fee is offset as provided by Exchange Act Rule 0-11(a)(2) and identify the filing for which the offsetting fee was paid previously. Identify the previous filing by registration statement number, or the Form or Schedule and the date of its filing.

1) | Amount Previously Paid: |

2) | Form, Schedule or Registration Statement No.: |

3) | Filing Party: |

4) | Date Filed: |

CARROLS RESTAURANT GROUP, INC.

968 James Street

Syracuse, NY 13203

________________________________________________

NOTICE OF ANNUAL MEETING OF STOCKHOLDERS

to be held August 29, 2019

________________________________________________

To the Stockholders of

Carrols Restaurant Group, Inc.:

You are invited to attend the annual meeting of stockholders, which we refer to as the “meeting”, of CARROLS RESTAURANT GROUP, INC., a Delaware corporation, which we refer to as “we”, “us”, “our”, the “Company” and “Carrols Restaurant Group”, at the principal executive offices of the Company located at 968 James Street, Syracuse, New York 13203 on Thursday, August 29, 2019, at 9:00 A.M. (EDT), for the following purposes:

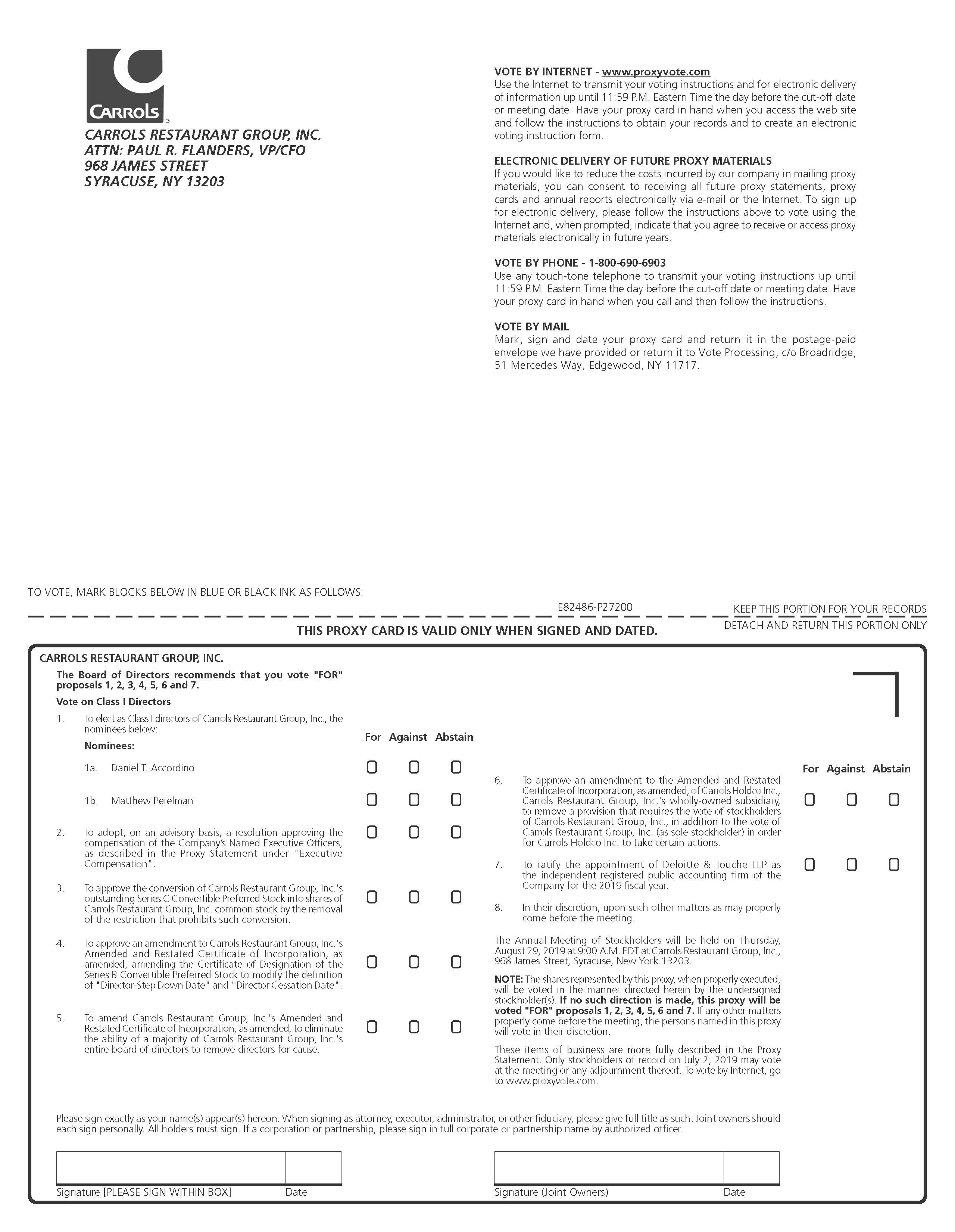

(1) | To elect two directors of the Company as Class I directors to serve for a term of three years and until their successors have been duly elected and qualified; |

(2) | To adopt, on an advisory basis, a resolution approving the compensation of the Company’s Named Executive Officers, as described in the Proxy Statement under “Executive Compensation”; |

(3) | To approve the conversion of our outstanding Series C Convertible Preferred Stock into shares of our common stock by removal of the restriction that prohibits such conversion; |

(4) | To approve an amendment to the Company’s Amended and Restated Certificate of Incorporation, as amended, amending the Certificate of Designation of the Series B Convertible Preferred Stock to modify the definition of “Director-Step Down Date” and “Director Cessation Date”; |

(5) | To amend our Amended and Restated Certificate of Incorporation, as amended, to eliminate the ability of a majority of our entire board of directors to remove directors for cause; |

(6) | To approve an amendment to the Amended and Restated Certificate of Incorporation, as amended, of Carrols Holdco Inc., Carrols Restaurant Group’s wholly-owned subsidiary, to remove a provision that requires the vote of stockholders of Carrols Restaurant Group, in addition to the vote of Carrols Restaurant Group (as sole stockholder) in order for Carrols Holdco Inc. to take certain actions; |

(7) | To ratify the appointment of Deloitte & Touche LLP as the independent registered public accounting firm of the Company for the 2019 fiscal year; and |

(8) | To consider and act upon such other matters as may properly come before the meeting. |

Only stockholders of record at the close of business on July 2, 2019, which we refer to as the “record date”, are entitled to receive notice of, and to vote at, the meeting, and at any adjournment or adjournments thereof. A list of our stockholders as of the close of business on July 2, 2019 will be available for inspection during business hours for ten days prior to the meeting at our principal executive offices located at 968 James Street, Syracuse, New York 13203.

If you are a stockholder of record, the inspector of election will have your name on a list and you will be able to gain entry to the meeting upon presentation of some form of government-issued photo identification such as a driver’s license, state-issued ID card or passport. If you are not a stockholder of record, but hold shares through a broker, trustee or nominee, you must provide proof of beneficial ownership as of the record date, such as an account statement or similar evidence of ownership, along with a form of photo identification referred to above. If you do not comply with the procedures outlined above, you will not be admitted to the meeting.

We are taking advantage of the Securities and Exchange Commission rule that allows us to deliver our proxy materials (which include the proxy statement included with this notice, our 2018 annual report and form of proxy card) to stockholders via the Internet. As a result, our stockholders will receive a mailing containing only a notice of the meeting instead of paper copies of our proxy materials.

Your vote is important. Whether or not you plan to attend the meeting, please review our proxy materials and request a proxy card to sign, date and return or submit your proxy by telephone or through the Internet. If you attend the meeting in person, you may, if you desire, revoke your proxy and choose to vote in person even if you had previously sent in your proxy card or voted by telephone or the Internet.

By order of the Board of Directors, |

|

WILLIAM E. MYERS, |

Vice President, General Counsel and Secretary |

Syracuse, New York

July 17, 2019

IMPORTANT NOTICE REGARDING THE AVAILABILITY OF PROXY MATERIALS FOR

THE 2019 ANNUAL MEETING OF STOCKHOLDERS TO BE HELD ON AUGUST 29, 2019

The Company’s Proxy Statement for the 2019 Annual Meeting of Stockholders is available at www.proxyvote.com.

CARROLS RESTAURANT GROUP, INC.

968 James Street

Syracuse, NY 13203

____________________________________________

PROXY STATEMENT FOR ANNUAL MEETING OF STOCKHOLDERS

August 29, 2019

________________________________________________

This Proxy Statement is furnished in connection with the solicitation of proxies by the board of directors, also referred to as the “board of directors” or the “board”, of CARROLS RESTAURANT GROUP, INC., a Delaware corporation, to be used at the annual meeting of stockholders, which we refer to as the “meeting”, of the Company which will be held at the principal executive offices of the Company located at 968 James Street, Syracuse, New York 13203 on Thursday, August 29, 2019, at 9:00 A.M. (EDT), and at any adjournment or adjournments thereof. Only stockholders of record at the close of business on July 2, 2019, which we refer to as the “record date”, will be entitled to vote at the meeting.

All references in this Proxy Statement to “Carrols Restaurant Group”, the “Company”, “we”, “us” and “our” refer to Carrols Restaurant Group, Inc.

Pursuant to the “notice and access” rules adopted by the Securities and Exchange Commission, which we refer to as the “SEC”, we have elected to provide access to our proxy materials (which include this proxy statement, our 2018 annual report and form of proxy) via the Internet. A Notice of Internet Availability of Proxy Materials, which we refer to as the “notice” will be mailed to our stockholders of record and beneficial owners (stockholders who own their stock through a nominee such as a bank or broker). The document will instruct stockholders on how to access the proxy materials on a secure website referred to in the notice or how to request printed copies.

In addition, by following the instructions in the notice, stockholders may request to receive proxy materials in printed form by mail or electronically by e-mail on an ongoing basis. Choosing to receive your future proxy materials by e-mail will save us the cost of printing and mailing documents to you. If you choose to receive future proxy materials by e-mail, you will receive an e-mail next year with instructions containing a link to those materials and a link to the proxy voting site. Your election to receive proxy materials by e-mail will remain in effect until you terminate it.

Your vote is important. Your shares can be voted at the meeting only if you are present in person or represented by proxy. Even if you plan to attend the meeting, we urge you to authorize your proxy in advance. You may complete your proxy and authorize your vote by proxy over the Internet or by telephone. In addition, if you received paper copies of the proxy materials by mail, you can also complete your proxy and authorize your vote by mail by following the instructions on the proxy card. Completing your proxy and authorizing your vote by proxy over the Internet, by telephone or by written proxy card will ensure your representation at the meeting regardless of whether you attend in person.

We encourage you to complete your proxy and authorize your vote by proxy electronically by going to the website www.proxyvote.com and entering your 12-digit control number located on your proxy card to create an electronic voting instruction form or complete your proxy and authorize your vote by calling the toll-free number (for residents of the United States and Canada) listed on your notice and proxy card. Please have your notice or proxy card in hand when going online or calling. If you complete your proxy and authorize your vote by proxy electronically over the Internet, you do not need to return your proxy card. If you choose to complete your proxy by mail, simply mark your proxy card, and then date, sign and return it in the postage-paid envelope provided.

If you hold your shares beneficially in street name through a nominee (such as a bank or broker), you may be able to complete your proxy and authorize your vote by proxy by telephone or the Internet as well as by mail. You should follow the instructions you receive from your nominee to vote these shares.

1

You may revoke your proxy at any time before it is voted at the meeting by:

• | properly executing and delivering a later-dated proxy (including a telephone or Internet proxy authorization); |

• | voting by ballot at the meeting; or |

• | sending a written notice of revocation to the inspector of election in care of the Corporate Secretary of the Company at the address listed above. |

Unless so revoked, the shares represented by proxies will be voted at the meeting. The shares represented by the proxies solicited by our board of directors will be voted in accordance with the directions given in the proxies, but if no direction is given, such shares will be voted (i) FOR the election of the two named director nominees as Class I directors, (ii) FOR, on an advisory basis, the approval of the non-binding resolution on the compensation of the Company’s Named Executive Officers as described in the Company’s proxy statement under “Executive Compensation”, (iii) FOR the approval of the conversion of our outstanding Series C Convertible Preferred Stock, par value $0.01 per share (the “Series C Preferred Stock”), into shares of our common stock, par value $0.01 per share, which we refer to as our “common stock” by the removal of the restriction that prohibits such conversion (the “Issuance Restriction”), (iv) FOR the approval of an amendment to the Company’s Amended and Restated Certificate of Incorporation, as amended, amending the Certificate of Designation of the Series B Convertible Preferred Stock, par value $0.01 per share (the “Series B Preferred Stock”) to modify the definition of “Director-Step Down Date” and “Director Cessation Date”, (v) FOR the approval of an amendment to our Amended and Restated Certificate of Incorporation, as amended, to eliminate the ability of a majority of our entire board of directors to remove directors for cause, (vi) FOR the approval of an amendment to the Amended and Restated Certificate of Incorporation, as amended, of Carrols Holdco Inc. (“Carrols Holdco”), Carrols Restaurant Group’s wholly-owned subsidiary, to remove a provision that requires the vote of stockholders of Carrols Restaurant Group, in addition to the vote of Carrols Restaurant Group (as sole stockholder) in order for Carrols Holdco to take certain actions and (vii) FOR the ratification of the appointment of Deloitte & Touche LLP, which we refer to as "Deloitte", as the independent registered public accounting firm of the Company for the 2019 fiscal year.

Stockholders vote at the meeting by casting ballots (in person or by proxy) which are tabulated by a person who is appointed by the board of directors before the meeting to serve as inspector of election at the meeting and who has executed and verified an oath of office. The affirmative vote of (i) a majority of the shares voting with respect to a director nominee (excluding abstentions) is required to elect such director nominee to the board of directors, (ii) a majority of the shares present at the meeting and entitled to vote on the subject matter is required to approve, on an advisory basis, the non-binding resolution on the compensation of the Company’s Named Executive Officers as described in the Company’s proxy statement under “Executive Compensation”, (iii), a majority of the shares present at the meeting and entitled to vote on the subject matter is required to approve the conversion of our outstanding Series C Preferred Stock into shares of our common stock by the removal of the restriction that prohibits such conversion, (iv) a majority of the outstanding shares of our common stock, together with our Series B Preferred Stock (voting on an as-converted basis), voting together as a single class is required to approve an amendment to our Amended and Restated Certificate of Incorporation, as amended, amending the Certificate of Designation of the Series B Preferred Stock to modify the definition of “Director-Step Down Date” and “Director Cessation Date”, (v) sixty-six and two-thirds percent (66 ⅔%) of the outstanding shares of our common stock, together with our Series B Preferred Stock (voting on an as-converted basis), voting together as a single class is required to approve the amendment to our Amended and Restated Certificate of Incorporation, as amended, to eliminate the ability of a majority of our entire board of directors to remove directors for cause, (vi) a majority of the outstanding shares of our common stock, together with our Series B Preferred Stock (voting on an as-converted basis), voting together as a single class is required to approve an amendment to the Amended and Restated Certificate of Incorporation, as amended, of Carrols Holdco, Carrols Restaurant Group’s wholly-owned subsidiary, to remove a provision that requires the vote of stockholders of Carrols Restaurant Group, in addition to the vote of Carrols Restaurant Group (as sole stockholder) in order for Carrols Holdco to take certain actions, (vii) a majority of the shares present at the meeting and entitled to vote on the subject matter is required to ratify the selection of Deloitte & Touche LLP as our independent registered public accounting firm for the 2019 fiscal year and (viii) a majority of the shares present at the meeting and entitled to vote on the subject matter is required to approve any other business which may properly come before the meeting. Abstentions and broker “non-votes” are included in the determination of the number of shares present at the meeting for quorum purposes. Abstentions will count as a vote against the proposals, other than for the election of directors. Broker “non-votes” are not counted in the tabulations of the votes cast or present

2

at the meeting and entitled to vote on any of the proposals and therefore will have no effect on the outcome of the proposals.

If your shares are held in “street name”, you have the right to direct your broker, bank or nominee how to vote. If you do not provide voting instructions, under the New York Stock Exchange rules, your broker, bank or nominee may only vote shares on discretionary matters. A broker “non-vote” occurs when a nominee holding shares for a beneficial owner does not vote on a particular proposal because the nominee does not have discretionary voting power with respect to that item and has not received instructions from the beneficial owner. Proposal 7 is considered a discretionary item and may be voted in the absence of instructions. Proposals 1, 2, 3, 4, 5 and 6 are non-discretionary items, and your broker, bank or nominee may not vote your shares on these items in the absence of voting instructions.

Our principal executive offices are located at 968 James Street, Syracuse, New York 13203. The approximate date on which the Notice was first sent or given to stockholders was on or about July 17, 2019.

On May 30, 2012, we and Carrols LLC, our indirect wholly-owned subsidiary, which we refer to as “Carrols LLC”, purchased 278 of Burger King Corporation’s (“BKC”) company-owned restaurants, which we refer to as the “2012 acquired restaurants”, located in Ohio, Indiana, Kentucky, Pennsylvania, North Carolina, South Carolina and Virginia, which we refer to as the “2012 acquisition”. As part of the consideration paid to BKC in the 2012 acquisition, on May 30, 2012, Carrols Holdco (formerly Carrols Restaurant Group, Inc.) issued 100 shares of its Series A Convertible Preferred Stock, par value $0.01 per share (“Series A Preferred Stock”), to BKC. In 2018, BKC exchanged the Series A Preferred Stock for Carrols Holdco's Series B Convertible Preferred Stock, par value $0.01 per share (the “Carrols Holdco Series B Preferred Stock”), with substantially the same powers, preferences and rights of the shares of Series A Preferred Stock, except to provide that such shares will be transferrable by BKC solely to certain of its affiliates or subsidiaries.

On February 19, 2019, Carrols Holdco, the Company, GRC MergerSub Inc., a wholly owned subsidiary of Carrols Holdco (“Carrols Merger Sub”), and GRC MergerSub LLC, a wholly owned subsidiary of Carrols Holdco (“Carrols CFP Merger Sub”) entered into an Agreement and Plan of Merger (the “Merger Agreement”) with Cambridge Franchise Partners, LLC (“CFP”), Cambridge Holdings, LLC, a wholly owned subsidiary of CFP (“Cambridge Holdings”), and New CFH, LLC, a wholly owned subsidiary of Cambridge Holdings (“New CFH”), pursuant to which the Company agreed to purchase the business of the subsidiaries of Cambridge Holdings, which included 165 Burger King® restaurants, 55 Popeyes® restaurants, six convenience stores and certain real property, through (i) a merger of Carrols Merger Sub and Carrols Holdco, with Carrols Holdco as the surviving entity, which resulted in Carrols Holdco becoming a wholly-owned subsidiary of the Company (the “Holding Company Reorganization”) and (ii) the merger of Carrols CFP Merger Sub and New CFH, with New CFH as the surviving entity (the “Cambridge Merger” and, together with the Holding Company Reorganization, the “Mergers”), in consideration for the issuance to Cambridge Holdings of 7,364,413 shares of our common stock (such shares, the “Cambridge Investor Shares”) and 10,000 shares of Series C Preferred Stock, each share of which is initially convertible into 745.04 shares of our common stock (or an aggregate of 7,450,402 shares of our common stock). The Mergers closed on April 30, 2019.

At the effective time of the Holding Company Reorganization, each share of Carrols Holdco common stock, par value $0.01 per share (the “Carrols Holdco Common Stock”), was automatically converted into one share of our common stock and each share of Carrols Holdco Series B Preferred Stock was automatically exchanged for one share of Series B Preferred Stock which has the same designations, rights, powers and preferences and the qualifications, limitations and restrictions as the corresponding share of Carrols Holdco Series B Preferred Stock.

VOTING SECURITIES

Our outstanding Series B Preferred Stock votes with our common stock on an as-converted basis on all matters properly brought before the meeting. Our outstanding Series C Preferred Stock does not have any voting rights. We had outstanding 44,371,515 shares of our common stock, 100 shares of Series B Preferred Stock and 10,000 shares of Series C Preferred Stock at the close of business on July 2, 2019. Each share of common stock is entitled to one vote on each matter as may properly be brought before the meeting. As of the record date, all 100 outstanding shares of Series B Preferred Stock are owned by BKC or its affiliate, Blue Holdco 1, LLC (“Blue Holdco” and together with BKC, the

3

“BKC Stockholders”). The BKC Stockholders are indirect subsidiaries and affiliates of Restaurant Brands International Inc. (“RBI”).

As of the record date, each share of Series B Preferred Stock is convertible into 94,145.8 fully paid and nonassessable shares of common stock (or an aggregate of 9,414,580 shares of our common stock). The Series B Preferred Stock votes with our common stock on an as-converted basis. As the owners of all of our outstanding shares of Series B Preferred Stock, the BKC Stockholders will be entitled to vote in the aggregate a total of 9,414,580 shares of common stock issuable upon the conversion of the Series B Preferred Stock on all matters properly brought before the meeting. All of such shares of common stock issuable upon conversion of the Series B Preferred Stock are included in the determination of the number of shares present at the meeting for quorum purposes.

Only stockholders of record at the close of business on July 2, 2019 will be entitled to vote.

4

PROPOSAL 1—ELECTION OF DIRECTORS

Our board of directors is divided into three classes of directors, with the classes as nearly equal in number as possible, each serving staggered three-year terms, except for the two Class B directors as described below. The terms of office of our Class I, Class II and Class III directors are:

• | Class I directors, whose term will expire at the meeting and when their successors are duly elected and qualified; |

• | Class II directors, whose term will expire at the Annual Meeting of Stockholders to be held in 2020 and when their successors are duly elected and qualified; and |

• | Class III directors, whose term will expire at the Annual Meeting of Stockholders to be held in 2021 and when their successors are duly elected and qualified. |

Our Class I directors are Daniel T. Accordino and Matthew Perelman; our Class II directors are Hannah S. Craven, Lawrence E. Hyatt, and Alexander Sloane and; and our Class III directors are David S. Harris and Deborah M. Derby. Additionally, in connection with the issuance of shares of Series B Preferred Stock held by the BKC Stockholders, since November 30, 2018, José E. Cil, Chief Executive Officer of RBI, the indirect parent company of BKC, has served as one of the two Class B directors (who replaced the two Class A directors upon the exchange of the Series A Preferred Stock for the Series B Preferred Stock) and since November 30, 2018 Matthew Dunnigan, Chief Financial Officer of RBI, the indirect parent company of BKC has served as the second of the Class B directors. From January 2015 until November 30, 2018, Mr. Cil served as one of the Class A directors. From October 2013 until February 2018, Alexandre Macedo, BKC’s President of North America, served as the second of the Class A directors. In February 2018, Mr. Macedo resigned as the second of the Class A directors and from February 2018 to November 30, 2018, Mr. Dunnigan served as the second of the two Class A directors. As further described under “Certain Relationships and Related Transactions—Series B Preferred Stock”, the terms of the Series B Preferred Stock exchanged for Series A Preferred Stock originally issued to BKC in connection with the 2012 acquisition provide that the BKC Stockholders are entitled to elect two Class B directors, subject to certain conditions. Each Class B director, in his capacity as a member of our board of directors, is afforded the same rights and privileges as the other members of our board of directors, including, without limitation, rights to indemnification, insurance, notice, information and the reimbursement of expenses.

In connection with the issuance of the Series C Preferred Stock, we entered into a Registration Rights and Stockholders' Agreement dated as of April 30, 2019 (the “Cambridge Registration Rights and Stockholders’ Agreement”) with Cambridge Holdings, pursuant to which the Company and our board of directors have agreed to take all necessary action so that: (i) until the date that Cambridge Holdings and the Permitted Affiliates (as defined in the Cambridge Registration Rights and Stockholders’ Agreement) hold shares of our common stock and together with shares of our common stock issuable upon the conversion of the Series C Preferred Stock (the “Conversion Common Stock”) constituting less than 14.5% of the total number of outstanding shares of our common stock (the “Cambridge Director Step-Down Date”), two individuals designated by Cambridge Holdings (each a “Cambridge Investor Director”) are nominated by our board of directors for election or re-election, as applicable, by the stockholders of the Company at each annual or special meeting of the stockholders at which Class I Directors or Class II Directors, as applicable, are subject to election or re-election, as applicable, as a Class I Director and a Class II Director, respectively; and (ii) from the Cambridge Director Step-Down Date to the date that Cambridge Holdings and the Permitted Affiliates hold shares of our common stock and Conversion Common Stock constituting less than 10% of the total number of outstanding shares of our common stock (the “Cambridge Director Cessation Date”), one Cambridge Investor Director is nominated by our board of directors for election or re-election, as applicable, by the stockholders of the Company at each annual or special meeting of the stockholders at which Class I Directors or Class II Directors, as applicable, are subject to election or re-election, as applicable, as a Class I Director or Class II Director. Pursuant to the Cambridge Registration Rights and Stockholders' Agreement, effective April 30, 2019, Matthew Perelman was appointed by our board of directors as a Class I Director and Alexander Sloane was appointed by our board of directors as a Class II Director. Each Cambridge Investor Director, in his capacity as a member of our board of directors, is afforded the same rights and privileges as the other members of our board of directors, including, without limitation, rights to indemnification, insurance, notice, information and the reimbursement of expenses.

5

Our board of directors is subject to a Mandatory Retirement Policy which provides that (i) effective February 16, 2017, any person (including any currently serving members of the board) shall not be eligible for election as a director of the board who: (A) is 75 years of age, which we refer to as the “Mandatory Retirement Age”, or older, or (B) would reach the Mandatory Retirement Age within one (1) year after the date on which he or she would stand for election to the board, and (ii) from and after the meeting, no person shall continue to serve as director of the board following the end of the calendar year that such person attains the Mandatory Retirement Age.

Two directors will be elected at the meeting as the Class I directors of the Company for a term of three years expiring at the Annual Meeting of Stockholders to be held in 2022 and until his or her successor shall have been elected and shall qualify. The election of a director requires the affirmative vote of a majority of the shares of common stock (including the shares of Series B Preferred Stock on an as-converted basis) voting with respect to a director nominee (excluding abstentions) in person or by proxy at the meeting. Each proxy received will be voted FOR the election of the nominees named below unless otherwise specified in the proxy. At this time, our board of directors knows of no reason why the nominees would be unable to serve. Except as disclosed in this Proxy Statement, there are no arrangements or understandings between any nominee and any other person pursuant to which such person was selected as a nominee.

Our Corporate Governance and Nominating Committee has reviewed the qualifications of the nominees for director and has recommended the nominees for election to the board of directors.

6

Director Nominees' Principal Occupation, Business Experience, Qualifications and Directorships

Name of Nominee | Principal Occupation | Age | Year Became a Director | |||

Daniel T. Accordino | CEO and President of Carrols Restaurant Group, Inc. | 68 | 1993 | |||

Matthew Perelman | Managing Partner of Garnett Station Partners | 32 | 2019 | |||

Daniel T. Accordino has been Chief Executive Officer of Carrols Restaurant Group since January 1, 2012 and Chairman of the board of directors since January 1, 2015. Mr. Accordino has been President and a director of Carrols Restaurant Group since February 1993 and was Chief Operating Officer of Carrols Restaurant Group from February 1993 to December 2011. Before that, Mr. Accordino served as Executive Vice President - Operations from December 1986 and as Senior Vice President of Carrols Corporation, our wholly owned subsidiary, which we refer to as “Carrols”, from April 1984. From 1979 to April 1984, he was Vice President of Carrols responsible for restaurant operations, having previously served as Assistant Director of Restaurant Operations. Mr. Accordino has been an employee of ours since 1972.

Mr. Accordino’s experience as our Chairman of the board of directors since January 1, 2015, Chief Executive Officer since January 1, 2012, as a director and President since 1993, past experience as our Chief Operating Officer from 1993 to 2011 and as an employee of the Company in various capacities since 1972 gives him outstanding skills and insight into our challenges as well as extensive knowledge of the restaurant industry. Mr. Accordino brings to the board significant leadership, management, operational, financial and brand management experience.

Matthew Perelman has served as a director since April 30, 2019. He is a Co-Founder and Managing Partner of Garnett Station Partners, an investment firm focused on retail and consumer companies. Prior to founding Garnett Station Partners in September 2013, Mr. Perelman worked at L Catterton, a large consumer-focused private equity fund, from June 2011 to June 2013. Prior to L Catterton, Mr. Perelman worked in the Investment Banking Division of Citigroup from June 2009 to June 2011, where he focused on consumer and retail M&A and financings. Mr. Perelman serves on the boards of Garnett Station Partners’ portfolio companies.

Mr. Perelman brings significant experience with strategic, investment, and financial issues of retail and restaurant companies in connection with his employment at Garnett Station Partners.

The board of directors unanimously recommends a vote FOR the election of each of the named Class I nominees to our board of directors, Daniel T. Accordino and Matthew Perelman. Proxies received in response to this solicitation will be voted FOR the election of each of the named Class I nominees to our board of directors unless otherwise specified in the proxy.

Principal Occupation, Business Experience, Qualifications and Directorships of Other Members of the Board of Directors

The following table sets forth information with respect to each of the members of our board of directors, whose term extends beyond the meeting, including the Class of such director and the year in which each such director’s term will expire.

Name | Age | Year Became a Director | Year Term Expires and Class | |||

Hannah S. Craven | 53 | 2015 | 2020 Class II | |||

Lawrence E. Hyatt | 64 | 2017 | 2020 Class II | |||

Alexander Sloane | 32 | 2019 | 2020 Class II | |||

David S. Harris | 59 | 2012 | 2021 Class III | |||

Deborah M. Derby | 55 | 2018 | 2021 Class III | |||

José E. Cil | 49 | 2015 | 2019 Class B | |||

Matthew Dunnigan | 35 | 2018 | 2019 Class B | |||

7

Directors

Hannah S. Craven has served as a director since March 27, 2015. Ms. Craven is a co-founder and partner of Stone-Goff Partners LLC ("Stone-Goff"), a private equity firm that focuses on investments in the consumer, business services, media, education, information, and retail/e-commerce industries. Prior to founding Stone-Goff and its predecessor fund in 2006, Ms. Craven was a Managing Director and General Partner of Sandler Capital Management from 1993 until 2006, a private equity firm specializing in investments in the media, communications, and information services industries, where she served as a key investment professional in five sequential private equity partnerships, was a general partner of its long/short hedge fund, and served on the Investment Advisory Board of a high yield CBO. Ms. Craven has over 20 years of experience investing in private equity transactions. Ms. Craven serves on several boards of directors of private portfolio companies of Stone-Goff.

Ms. Craven brings significant experience with the strategic, financial and operational issues of consumer and services companies in connection with her service on the boards of a number of her current and prior firms' past and current portfolio companies.

Lawrence E. Hyatt has served as a director since June 8, 2017. Mr. Hyatt has served as a director of Citi Trends Inc., a publicly traded retail apparel company from 2006 until 2017 where he also served as Chairman of the Audit Committee, and as a member of the Compensation Committee and the Nominating and Corporate Governance Committee for Citi Trends Inc. Mr. Hyatt served as the Senior Vice President and Chief Financial Officer of Cracker Barrel Old Country Store, Inc., a publicly traded restaurant and retail company, from January 2011 until July 1, 2016. From 2004 through 2010, Mr. Hyatt served as the Chief Financial Officer, Secretary and Treasurer of O’Charley’s Inc., a private multi-concept restaurant company. Mr. Hyatt also served as Interim Chief Executive Officer of O’Charley’s Inc. from February 2009 through June 2009. Mr. Hyatt served as the Executive Vice President and Chief Financial Officer of Cole National Corporation, a specialty retailer, from 2002 to 2004, as Chief Financial and Restructuring Officer of PSINet Inc., an internet service provider, from 2000 to 2002, as Chief Financial Officer of HMS Host Corporation, a subsidiary of Autogrill S.P.A., from 1999 to 2000, and as Chief Financial Officer of Sodexho Marriott Services, Inc. and its predecessor company from 1989 to 1999.

Mr. Hyatt brings significant experience with the strategic, financial, and operational issues of restaurant companies and food service companies in connection with his service as an executive officer and on the boards of a number of public and private retail consumer companies.

David S. Harris has served as a director since May 7, 2012. He has served as President of Grant Capital, Inc., a private investment company, since January 2002. From May 2001 until December 2001, Mr. Harris served as a Managing Director in the investment banking division of ABN Amro Securities LLC. From September 1997 until May 2001, Mr. Harris served as a Managing Director and Sector Head of the Retail, Consumer and Leisure Group of ING Barings LLC, a financial institution. From 1986 to 1997, Mr. Harris served in various capacities as a member of the investment banking group of Furman Selz LLC. Mr. Harris is a director of REX American Resources Corporation, Spectrum Brands Holdings, Inc. and, until its sale in December 2015, was a director of Steiner Leisure Limited. Mr. Harris serves as Lead Director and Chairman of the Audit and Compensation Committees of REX American Resources Corporation and served on the Audit Committee and was Chairman of the Compensation Committee and Special Committee of independent board members formed to consummate the sale of Steiner Leisure Limited.

Mr. Harris brings significant experience with the strategic, financial and operational issues of retail and consumer companies in connection with his service on the boards of a number of public and private companies.

Deborah M. Derby has served as a director since June 7, 2018. Ms. Derby serves as President of Horizon Group USA, a privately held retailer of craft components, activity kits and impulse and seasonal items since April 2016. Prior to being named President, from November 2015 to March 2016, Ms. Derby served as a consultant to Horizon Group USA. Ms. Derby also currently serves as a member of Horizon’s advisory board of directors. Ms. Derby previously served as Vice Chairman, Executive Vice President of Toys “R” Us from March 2013 to August 2015. Prior to her rejoining Toys “R” Us, Ms. Derby consulted for Kenneth Cole Productions, Inc., beginning in September 2012. Ms. Derby previously served as Chief Administrative Officer for Toys “R” Us from February 2009 to February 2012. Ms. Derby joined Toys “R” Us in 2000 as Vice President, Human Resources and held positions of increasing responsibility during her 11 years there, including Corporate Secretary, Executive Vice President, Human Resources, Legal & Corporate Communications and President, Babies “R” Us. Prior to joining Toys “R” Us, Ms. Derby spent eight years at Whirlpool

8

Corporation with her last position there as Corporate Director Compensation & Benefits. Ms. Derby also has experience as an attorney specializing in employment law and as a financial analyst with The Goldman Sachs Group, Inc. Ms. Derby has been a director on the Board of Directors of the Vitamin Shoppe Inc. (NYSE:VSI) since 2012 where she serves as the Chair of the Compensation Committee and a member of the Nomination and Governance Committee.

Ms. Derby brings significant experience with the strategic, financial, and operational issues of consumer retail companies in connection with her service on the boards of public and private companies and as a senior executive officer of several retail and consumer goods companies.

Alexander Sloane is a Co-Founder and Managing Partner of Garnett Station Partners, an investment firm focused on retail and consumer companies. Prior to founding Garnett Station Partners in September 2013, Mr. Sloane worked in private equity at Apollo Global Management from 2011 to 2013. Prior to Apollo, Mr. Sloane worked in Investment Banking at Goldman Sachs from 2009 to 2011. Mr. Sloane serves on the boards of Garnett Station Partners’ portfolio companies.

Mr. Sloane brings significant experience with strategic, investment, and financial issues of retail and restaurant companies in connection with his employment at Garnett Station Partners.

José E. Cil has served as a Class B director since November 30, 2018 and served as Class A director from January 28, 2015 until November 30, 2018. Mr. Cil was appointed Chief Executive Officer of RBI effective January 23, 2019. Mr. Cil served as Executive Vice President and President, Burger King, of RBI, from December 15, 2014 until January 23, 2019. Mr. Cil served as Executive Vice President and President of Europe, the Middle East and Africa for Burger King Worldwide Inc. and its predecessor from November 2010 until December 2014. Mr. Cil also served as Vice President and Regional General Manager for Wal-Mart Stores, Inc. in Florida from February 2010 to November 2010. From September 2008 to January 2010, Mr. Cil served as Vice President of Company Operations of BKC and from September 2005 to September 2008, he served as Division Vice President, Mediterranean and NW Europe Divisions, EMEA of a subsidiary of BKC.

Mr. Cil brings significant experience with the strategic, financial, and operational issues of restaurant companies in connection with his employment as an executive officer of RBI.

Matthew Dunnigan has served a Class B director since November 30, 2018 and served as a Class A director from February 5, 2018 until November 30, 2018. Mr. Dunnigan has been Chief Financial Officer of RBI since January 22, 2018. Mr. Dunnigan served as RBI’s Treasurer from October 2014 to January 22, 2018. Prior to joining RBI, Mr. Dunnigan served as Vice President of Crescent Capital Group LP from September 2013 to October 2014. Mr. Dunnigan served for three years as an investment professional for H.I.G. Capital from July 2008 to June 2011. Prior to that Mr. Dunnigan worked in investment banking with Bear, Stearns & Co., Inc., for two years.

Mr. Dunnigan brings significant experience with the strategic, financial and operational issues of restaurant companies in connection with his employment as an executive officer of RBI.

Information Regarding Executive Officers

Name | Age | Position | ||

Daniel T. Accordino | 68 | Chairman of the Board, Chief Executive Officer and President | ||

Paul R. Flanders | 62 | Vice President, Chief Financial Officer and Treasurer | ||

Richard G. Cross | 56 | Vice President, Real Estate | ||

William E. Myers | 63 | Vice President, General Counsel and Secretary | ||

Gerald J. DiGenova | 62 | Vice President, Human Resources | ||

Nathan Mucher | 47 | Vice President, Chief Information Officer | ||

For biographical information regarding Daniel T. Accordino, please see “— Director Nominees’ Principal Occupation, Business Experience, Qualifications and Directorships”.

Paul R. Flanders has been Vice President, Chief Financial Officer and Treasurer since April 1997. From May 7, 2012 until July 16, 2012, Mr. Flanders also served as the Interim Chief Financial Officer of Fiesta Restaurant Group. Before joining us, he was Vice President-Corporate Controller of Fay’s Incorporated, a retail chain, from 1989 to 1997,

9

and Vice President-Corporate Controller for Computer Consoles, Inc., a computer systems manufacturer, from 1982 to 1989. Mr. Flanders was also associated with the accounting firm of Touche Ross & Co. from 1977 to 1982.

Richard G. Cross has been Vice President, Real Estate since July 2001. Mr. Cross was Director of Real Estate from 1994 until July 2001. Mr. Cross served as a Real Estate Manager from 1993 until 1994 and as a Real Estate Representative from 1987 until 1993. Mr. Cross joined us in May 1984 and held various positions in the Purchasing Department until 1987.

William E. Myers has been General Counsel and Secretary since May 7, 2012. He was appointed Vice President in July 2001. Mr. Myers served as Associate General Counsel from March 2001 through May 7, 2012. Before joining us, Mr. Myers was engaged in private practice beginning in 1982.

Gerald J. DiGenova has been Vice President, Human Resources since July 2001. Mr. DiGenova was Director of Human Resources from January 1996 until June 2001. Mr. DiGenova served as Director of Safety and Risk Management from 1992 until December 1995 and Personnel Manager from January 1985 until January 1992. Mr. DiGenova has been an employee of ours since 1973, when he began as an hourly restaurant team member.

Nathan Mucher has been Vice President, Chief Information Officer since November 2018. Before joining us, Mr. Mucher served as Vice President, Information Technology for Krispy Kreme Doughnuts from 1999 until 2018, as a consultant for Novartis Animal Health from July 1998 to December 1998, as System Analyst for JS Walker & Company, an information technology consulting service, from 1996 until 1998, and as senior programmer for William James and Associates, an information technology consulting service from 1994 until 1996.

Information Regarding the Board of Directors and Committees

Family Relationships

There are no family relationships between any of our executive officers or directors.

Independence of Directors

During the fiscal year ended December 30, 2018, our board of directors met or acted by unanimous consent on eight occasions. During the fiscal year ended December 30, 2018, each of the directors attended at least 75% of the aggregate number of meetings of the board of directors and of any committees of the board of directors on which they served. We do not have a policy on attendance by directors at our annual meeting of stockholders. One director serving at such time attended our 2018 annual meeting of stockholders.

As required by the listing standards of NASDAQ, a majority of the members of our board of directors must qualify as “independent”, as affirmatively determined by our board of directors. Our board of directors determines director independence based on an analysis of such listing standards and all relevant securities and other laws and regulations regarding the definition of “independent.”

Consistent with these considerations, after review of all relevant transactions and relationships between each director, any of his or her family members, and us, our executive officers and our independent registered public accounting firm, the board of directors has affirmatively determined that a majority of our board of directors is comprised of independent directors. Our independent directors pursuant to NASDAQ listing standards for all purposes other than serving on our Audit Committee are Hannah S. Craven, Deborah M. Derby, David S. Harris, Lawrence E. Hyatt, Matthew Perelman and Alexander Sloane.

Committees of the Board

The standing committees of our board of directors consist of an Audit Committee, a Compensation Committee, a Corporate Governance and Nominating Committee, and a Finance Committee. Our board of directors may also establish from time to time any other committees that it deems necessary or advisable.

10

Audit Committee

Our Audit Committee consists of Hannah S. Craven, David S. Harris and, Lawrence E. Hyatt (Chair). All three members of the Audit Committee satisfy the independence requirements of Rule 10A-3 of the Securities Exchange Act of 1934, as amended, which we refer to as the “Exchange Act”, and Rule 5605 of the NASDAQ listing standards. Each member of our Audit Committee is financially literate and the board of directors has determined that Mr. Hyatt is the Audit Committee “financial expert” within the meaning of Item 407 of Regulation S-K of the Securities Act of 1933, as amended, which we refer to as the “Securities Act” , and has the financial sophistication required under the NASDAQ listing standards. Our Audit Committee, among other things:

• | reviews our annual and interim financial statements and reports to be filed with the SEC; |

• | monitors our financial reporting process and internal control system; |

• | appoints and replaces our independent outside auditors from time to time, determines their compensation and other terms of engagement and oversees their work; |

• | oversees the performance of our internal audit function; |

• | conducts a review of all related party transactions for potential conflicts of interest and approves all such related party transactions; |

• | establishes procedures and monitors the receipt, retention and treatment of complaints regarding accounting, internal accounting controls or auditing matters and the confidential anonymous submission by employees of concerns regarding questionable accounting or auditing matters; and |

• | oversees our compliance with legal, ethical and regulatory matters. |

The Audit Committee has the sole and direct responsibility for appointing, evaluating and retaining our independent registered public accounting firm and for overseeing their work. All audit services to be provided to us and all permissible non-audit services, other than de minimis non-audit services, to be provided to us by our independent registered public accounting firm are approved in advance by our Audit Committee. During the fiscal year ended December 30, 2018, the Audit Committee met or acted by unanimous consent on seven occasions. The Audit Committee has adopted a formal written Audit Committee charter that complies with the requirements of the Exchange Act and the NASDAQ listing standards. A copy of the Audit Committee charter is available on the investor relations section of our website at www.carrols.com.

11

Audit Committee Report

Management has primary responsibility for preparing the Company's financial statements and establishing an effective system of internal control over financial reporting and disclosure controls and procedures. The independent registered public accounting firm is responsible for expressing an opinion as to the conformity of the Company's financial statements with generally accepted accounting principles and as to the effectiveness of the Company's internal control over financial reporting based on their audit. The Audit Committee oversees on behalf of the board (i) the accounting, financial reporting and internal control processes of the Company and (ii) the audits of the financial statements and internal controls of the Company.

The Audit Committee operates under a written charter adopted by the board which sets forth its responsibilities and duties. The Audit Committee charter is available on the Company’s Investor Relations website at https://investor.carrols.com under “Corporate Governance > Audit Committee Charter.”

The Company has an Internal Audit Department that reports to the Audit Committee. The Audit Committee reviews and approves the internal audit plan once a year and receives periodic updates of internal audit activity in meetings held at least quarterly throughout the year. Updates include discussions of audit project results, as well as quarterly assessments of internal controls.

The Audit Committee has met and held discussions with management and Deloitte & Touche LLP (“Deloitte”), the Company’s independent registered public accounting firm. Management represented to the Audit Committee that the Company’s financial statements for the year ended December 30, 2018 were prepared in accordance with generally accepted accounting principles. The Audit Committee discussed the financial statements with both management and Deloitte. The Audit Committee also discussed with Deloitte the matters required to be discussed pursuant to Auditing Standard No. 1301, Communications with Audit Committees, adopted by the Public Company Accounting Oversight Board (“PCAOB”), and PCAOB's Auditing Standard No. 2201, “An Audit of Internal Control Over Financial Reporting That is Integrated with an Audit of Financial Statements.” The Audit Committee also discussed with Deloitte the firm’s independence from the Company and management, including the independent auditors’ written disclosures required by Ethics & Independence Rule No. 3526, Communication with Audit Committees Concerning Independence, adopted by the PCAOB.

The Audit Committee also discussed with Deloitte the overall scope and plans for the audit. The Audit Committee met with Deloitte both with and without management, to discuss the results of their examination, the evaluation of the Company’s internal controls and the overall quality of the Company’s financial reporting.

Management has completed its annual documentation, testing, and evaluation of the Company’s system of internal control over financial reporting in response to the requirements set forth in Section 404 of the Sarbanes-Oxley Act of 2002 and related regulations. The Audit Committee met periodically, both independently and with management, to review and discuss the Company’s progress in complying with Section 404, including PCAOB Auditing Standard No. 5 regarding the audit of the system of internal control over financial reporting. The Audit Committee also met periodically with Deloitte to discuss our internal controls and the status of the Company’s Section 404 compliance efforts. At the conclusion of the process, management provided the Audit Committee with a report on the effectiveness of the Company’s internal control over financial reporting. The Audit Committee continues to oversee the Company’s efforts related to its internal controls.

Based on the foregoing, we have recommended to the board of directors that the Company’s audited financial statements be included in its Annual Report on Form 10-K for the year ended December 30, 2018, for filing with the Securities and Exchange Commission.

Audit Committee |

Lawrence E. Hyatt, Chair |

Hannah S. Craven |

David S. Harris |

12

Compensation Committee

Our Compensation Committee consists of Hannah S. Craven, Deborah M. Derby, David S. Harris (Chair), Matthew Perelman, and Alexander Sloane. All five members of our Compensation Committee are “independent” as defined under Rule 5605 of the NASDAQ listing standards. The purpose of our Compensation Committee is to discharge the responsibilities of our board of directors relating to compensation of our executive officers. Our Compensation Committee, among other things:

• | provides oversight on the development and implementation of the compensation policies, strategies, plans and programs for our outside directors and disclosure relating to these matters; and |

• | reviews and approves the compensation of our Chief Executive Officer and the other executive officers of us and our subsidiaries. |

The processes and procedures that the Compensation Committee uses to determine executive officer compensation and outside directors’ compensation are described in the Compensation Discussion and Analysis included in this Proxy Statement.

In March 2016, the Compensation Committee engaged the services of Pearl Meyer, an outside independent compensation consultant, to assist it with a review of the compensation for executive officers and directors of the Company. The nature and scope of Pearl Meyer's assignment and the material elements of the instructions or directions given to Pearl Meyer with respect to the performance of their duties under the engagement are described in the Compensation Discussion and Analysis included in this Proxy Statement. We believe that the use of an independent compensation consultant provides additional assurance that our compensation programs are reasonable and consistent with our goals and objectives. The Compensation Committee may form one or more subcommittees, each of which shall take such actions as shall be delegated by the Compensation Committee.

The Compensation Committee has adopted a formal, written Compensation Committee charter that complies with SEC rules and regulations and the NASDAQ listing standards. During the fiscal year ended December 30, 2018, the Compensation Committee met or acted by unanimous consent on five occasions. A copy of the Compensation Committee charter is available on the investor relations section of our website at www.carrols.com.

Corporate Governance and Nominating Committee

Our Corporate Governance and Nominating Committee consists of Hannah S. Craven (Chair), David S. Harris, Lawrence E. Hyatt, Matthew Perelman, and Alexander Sloane. All of the members of our Corporate Governance and Nominating Committee are “independent” as defined under Rule 5605 of the NASDAQ listing standards. Our Corporate Governance and Nominating Committee, among other things:

• | establishes criteria for board and committee membership and recommends to our board of directors proposed nominees for election to the board of directors and for membership on committees of the board of directors; |

• | makes recommendations regarding proposals submitted by our stockholders; and |

• | makes recommendations to our board of directors regarding corporate governance matters and practices. |

The Corporate Governance and Nominating Committee has adopted a formal written Corporate Governance and Nominating Committee charter that complies with SEC rules and regulations and the NASDAQ listing standards. During the fiscal year ended December 30, 2018, the Corporate Governance and Nominating Committee met or acted by unanimous written consent on three occasions. A copy of the Corporate Governance and Nominating Committee charter is available on the investor relations section of our website at www.carrols.com.

13

Finance Committee

Our Finance Committee consists of David S. Harris, Lawrence E. Hyatt, Matthew Perelman, and Alexander Sloane. Paul Flanders, our Vice President, Chief Financial Officer and Treasurer, serves as a non-board advisor of the Finance Committee. Our Finance Committee, among other things:

• | reviews and provides guidance to our board of directors and management about policies relating to the Company’s working capital; stockholder dividends and distributions; share repurchases; significant investments; capital and debt issuances; material financial strategies and strategic investments; and other transactions or financial issues that management desires to have reviewed by the Finance Committee; and |

• | obtains or performs an annual evaluation of the Committee’s performance and makes applicable recommendations to the board of directors. |

Nominations For The Board Of Directors

The Corporate Governance and Nominating Committee of the board of directors considers director candidates based upon a number of qualifications. The qualifications for consideration as a director nominee vary according to the particular area of expertise being sought as a complement to the existing composition of the board. At a minimum, however, the Corporate Governance and Nominating Committee seeks candidates for director who possess:

• | the highest personal and professional ethics, integrity and values; |

• | the ability to exercise sound judgment; |

• | the ability to make independent analytical inquiries; |

• | willingness and ability to devote adequate time, energy and resources to diligently perform board and board committee duties and responsibilities; and |

• | a commitment to representing the long-term interests of the stockholders. |

In addition to such minimum qualifications, the Corporate Governance and Nominating Committee takes into account the following factors when considering a potential director candidate:

• | whether the individual possesses specific industry expertise and familiarity with general issues affecting our business; and |

• | whether the person would qualify as an “independent” director under SEC and NASDAQ rules. |

The Corporate Governance and Nominating Committee has not adopted a specific diversity policy with respect to identifying nominees for director. However, the Corporate Governance and Nominating Committee takes into account the importance of diversified board membership in terms of the individuals involved and their various experiences and areas of expertise.

The Corporate Governance and Nominating Committee shall make every effort to ensure that the board and its committees include at least the required number of independent directors, as that term is defined by applicable standards promulgated by NASDAQ and/or the SEC. Backgrounds giving rise to actual or perceived conflicts of interest are undesirable. In addition, prior to nominating an existing director for re-election to the board, the Corporate Governance and Nominating Committee will consider and review such existing director’s board and committee attendance and performance, independence, experience, skills and the contributions that the existing director brings to the board.

The Corporate Governance and Nominating Committee has in the past relied upon third party search firms to identify director candidates, and may employ such firms in the future if so desired. The Corporate Governance and Nominating Committee generally relies upon, receives and reviews recommendations from a wide variety of contacts, including current executive officers, directors, community leaders, and stockholders as a source for potential director candidates. The board retains complete independence in making nominations for election to the board.

The Corporate Governance and Nominating Committee will consider qualified director candidates recommended by stockholders in compliance with our procedures and subject to applicable inquiries. The Corporate Governance and Nominating Committee’s evaluation of candidates recommended by stockholders does not differ materially from its evaluation of candidates recommended from other sources. Pursuant to our amended and restated bylaws, as amended,

14

any stockholder may recommend nominees for director not less than 90 days nor more than 120 days in advance of the anniversary date of the immediately preceding annual meeting of stockholders, by writing to William E. Myers, Vice President, General Counsel and Secretary, Carrols Restaurant Group, Inc., 968 James Street, Syracuse, NY 13203, giving the name, Company stockholdings and contact information of the person making the nomination, the candidate’s name, address and other contact information, any direct or indirect holdings of our securities by the nominee, any information required to be disclosed about directors under applicable securities laws and/or stock exchange requirements, information regarding related party transactions with us, the nominee and/or the stockholder submitting the nomination, and any actual or potential conflicts of interest, the nominee’s biographical data, current public and private company affiliations, employment history and qualifications and status as “independent” under applicable securities laws and/or stock exchange requirements. All of these communications will be reviewed by our Secretary and forwarded to the Chairman of the Corporate Governance and Nominating Committee, for further review and consideration in accordance with this policy. Any such stockholder recommendation should be accompanied by a written statement from the candidate of his or her consent to be named as a candidate and, if nominated and elected, to serve as a director.

Board Leadership Structure and Role in Risk Oversight

Board Leadership

Mr. Accordino currently serves as Chairman of our board of directors and Chief Executive Officer and President. The board of directors has determined that having the roles of Chairman of the board of directors and Chief Executive Officer in the same individual is the appropriate leadership structure for the Company and in the best interest of our stockholders at this time. This structure promotes the execution of the strategic responsibilities of the board of directors and management because the Chief Executive Officer is the director most familiar with identifying strategic priorities and leading the discussion and execution of our strategy. Our board of directors reserves the right to determine from time to time how to configure the leadership of the board of directors and the Company in the way that best serves us and our stockholders. The board of directors believes that each of the possible leadership structures for a board has its particular pros and cons, which must be considered in the context of the specific circumstances, culture and challenges facing a company, and that such consideration falls squarely on the shoulders of a company’s board and necessitates a diversity of views and experiences. Our board of directors does not have a lead independent director.

The board recognizes that depending on the circumstances, other leadership models, such as a separate Chairman of the Board, might be appropriate. Accordingly, the board regularly reviews and reassesses its leadership structure.

Risk Oversight

Our board of directors believes that oversight of risk management is the responsibility of the full board, with support from its committees and senior management. The board of directors’ principal responsibility in this area is to ensure that sufficient resources, with appropriate technical and managerial skills, are provided throughout the Company to identify, assess and facilitate processes and practices to address material risks. We believe that the current leadership structure enhances the board of directors' ability to fulfill this oversight responsibility.

Some risks, particularly those relating to potential operating liabilities, the protection against physical loss or damage to our facilities, and the possibility of business interruption resulting from a large loss event, are contained and managed by legal contracts of insurance. Our insurance contracts are reviewed, managed and procured by our Risk Management and Legal departments along with our Chief Financial Officer to optimize their completeness and efficacy, and our Vice President of Human Resources (who is responsible for Risk Management) advises the board on matters relating to insurance as appropriate. Periodic presentations are made to the board to identify and discuss risks and the mitigation of risk and the board members, particularly the Audit Committee, assesses and oversees business risks as a component of their review of the business and financial activities of the Company.

Code of Ethics

We have adopted written codes of ethics applicable to our directors, officers and employees in accordance with the rules of the SEC and the NASDAQ listing standards. We make our codes of ethics available free of charge on the investor relations section of our website at www.carrols.com. We will disclose on our website amendments to or waivers from our codes of ethics in accordance with all applicable laws and regulations.

15

Section 16(a) Beneficial Ownership Reporting Compliance

Based upon a review of the filings furnished to us pursuant to Rule 16a-3(e) promulgated under the Exchange Act, and on representations from our executive officers and directors and persons who beneficially own more than 10% of our common stock, all filing requirements of Section 16(a) of the Exchange Act were complied with in a timely manner during the fiscal year ended December 30, 2018.

Stockholder Communications With The Board Of Directors

Any stockholder or other interested party who desires to communicate with our Chairman of the board of directors or any of the other members of the board of directors may do so by writing to: Board of Directors, c/o Daniel Accordino, Chairman of the board of directors, Carrols Restaurant Group, Inc., 968 James Street, Syracuse, NY 13203. Communications may be addressed to the Chairman of the Board, an individual director, a board committee, the non-management directors or the full board. Communications will then be distributed to the appropriate directors unless the Chairman determines that the information submitted constitutes “spam”, pornographic material and/or communications offering to buy or sell products or services.

16

SECURITY OWNERSHIP OF CERTAIN BENEFICIAL OWNERS

AND MANAGEMENT

The following table provides information regarding beneficial ownership of our common stock as of July 2, 2019 and to reflect the conversion of Series B Preferred Stock and the Series C Preferred Stock into shares of our common stock by:

• | each stockholder known by us to beneficially own more than 5% of our outstanding shares of common stock; |

• | each of our directors, nominees for director and Named Executive Officers (as defined in “Executive Compensation—Compensation Discussion and Analysis” herein) individually; and |

• | all directors and executive officers as a group. |

There were 44,371,515 shares of our common stock outstanding on July 2, 2019 (without giving effect to the conversion of Series B Preferred Stock or the conversion of the Series C Preferred Stock).

Unless noted otherwise, to our knowledge, each of the following persons listed below have sole voting and investment power with respect to the shares of common stock beneficially owned, except to the extent that authority is shared by spouses under applicable law.

The information contained in this table reflects “beneficial ownership” as defined in Rule 13d-3 of the Exchange Act. Beneficial ownership includes any shares to which the person has either sole or shared voting power or investment power and also any shares of common stock the individual has the right to acquire within 60 days following July 2, 2019 through the exercise any stock option or other right, including options to officers and directors authorized by board resolution, but not yet issued, (ii) shares of common stock issuable upon conversion of Series B Preferred Stock held by that person that were convertible on July 2, 2019 or convertible within 60 days following that date and (iii) assuming that Proposal 3 herein is approved by the requisite stockholders at the meeting, shares of common stock issuable upon conversion of Series C Preferred Stock held by that person that were convertible on July 2, 2019 or convertible within 60 days following that date. However, such shares are not considered outstanding for the purpose of computing the percentage ownership of any other person, nor is there any obligation to exercise any of the options, to convert the Series B Preferred Stock or to convert the Series C Preferred Stock (although in the event that Proposal 3 herein is approved by the requisite stockholders at the meeting, the Series C Preferred Stock will automatically convert into shares of our common stock). Except as otherwise indicated, the address for each beneficial owner is c/o Carrols Restaurant Group, Inc., 968 James Street, Syracuse, NY 13203.

17

Name and Address of Beneficial Owner | Amount and Nature of Beneficial Ownership | Percent of Class | Percent of Class Giving Effect to the Conversion of Series B Preferred Stock (1) | Percent of Class Giving Effect to the Conversion of Series B Preferred Stock and Series C Preferred Stock (2) | ||||||||

Restaurant Brands International, Inc. (3) | 9,414,580 | — | % | 17.5 | % | 15.4 | % | |||||

Restaurant Brands International Limited Partnership | ||||||||||||

Cambridge Franchise Holdings, LLC (4) | 14,814,815 | 16.6 | % | 13.7 | % | 24.2 | % | |||||

BlackRock, Inc. (5) | 2,942,825 | 6.6 | % | 5.5 | % | 4.8 | % | |||||

Dimensional Fund Advisors LP (6) | 2,355,229 | 5.3 | % | 4.4 | % | 3.8 | % | |||||

Private Capital Management, LLC (7) | 2,278,462 | 5.1 | % | 4.2 | % | 3.7 | % | |||||

Daniel T. Accordino (8) | 1,433,332 | 3.2 | % | 2.7 | % | 2.3 | % | |||||

Paul R. Flanders (9) | 364,844 | * | * | * | ||||||||

Richard G. Cross (10) | 186,199 | * | * | * | ||||||||

Gerald J. DiGenova (11) | 166,401 | * | * | * | ||||||||

William E. Myers (12) | 92,163 | * | * | * | ||||||||

David S. Harris | 64,115 | * | * | * | ||||||||

Hannah S. Craven | 41,091 | * | * | * | ||||||||

Lawrence E. Hyatt | 18,097 | * | * | * | ||||||||

Deborah M. Derby | 15,823 | * | * | * | ||||||||

José E. Cil (13) | — | — | % | — | % | — | % | |||||

Matthew Dunnigan (13) | — | — | % | — | % | — | % | |||||

Matthew Perelman (14) | 14,826,673 | 16.6 | % | 13.7 | % | 24.2 | % | |||||

Alexander Sloane (15) | 14,826,524 | 16.6 | % | 13.7 | % | 24.2 | % | |||||

All directors and executive officers as a group | 17,235,447 | 22.0 | % | 18.2 | % | 28.1 | % | |||||

_____

* | Less than 1.0%. |

(1) | Percentages calculated on the basis of a number of shares of our common stock outstanding equal to the sum of (i) 44,371,515, the number of shares of our common stock outstanding as of July 2, 2019 and (ii) 9,414,580, the number of shares of our common stock that would be issuable upon the conversion of all of the outstanding shares of Series B Preferred Stock. |

(2) | Percentages calculated on the basis of a number of shares of our common stock outstanding equal to the sum of (i) 44,371,515, the number of shares of our common stock outstanding as of July 2, 2019, (ii) 9,414,580, the number of shares of our common stock that would be issuable upon the conversion of all of the outstanding shares of Series B Preferred Stock and (iii) 7,450,402, the number of shares of our common stock that would be issuable upon the conversion of all of the outstanding shares of Series C Preferred Stock after giving effect to the removal of the Issuance Restriction. |

(3) | Information was obtained from a Schedule 13D/A (Amendment No. 2) filed on May 9, 2019 with the SEC. BKC and Blue Holdco, another affiliate of RBI, beneficially own an aggregate of 9,414,580 shares of our common stock issuable upon the conversion of shares of Series B Preferred Stock. RBI and Restaurant Brands International Limited Partnership (“RBI LP”) each has sole voting power over 9,414,580 shares, sole dispositive power over 9,414,580 shares and shared voting and shared dispositive power over 0 shares. The address for RBI and RBI LP is 130 King Street West, Suite 300, P.O. Box 399, Toronto, Ontario M5X 1E1 Canada. |

(4) | Information was obtained from a Schedule 13D filed on May 10, 2019 with the SEC. Cambridge Holdings and CFP beneficially own an aggregate of 7,364,413 shares of our common stock and 7,450,402 shares of our common stock, issuable upon the conversion of shares of the Series C Preferred Stock after giving effect to the removal of the Issuance Restriction. The address for each of Cambridge Holdings and CFP is 853 Broadway, Suite 2014, New York, New York 10003. |

(5) | Information was obtained from a Schedule 13G/A (Amendment No. 2) filed on February 4, 2019 with the SEC. The address for BlackRock, Inc. is 55 East 52nd Street, New York, NY 10055. BlackRock, Inc. has sole voting power over 2,763,726 shares, sole dispositive power over 2,942,825 shares and shared voting and shared dispositive power over 0 shares. |

18

(6) | Information was obtained from a Schedule 13G/A (Amendment No. 1) filed on February 8, 2019 with the SEC. The address for Dimensional Fund Advisors LP is Building One, 6300 Bee Cave Road, Austin, Texas, 78746. Dimensional Fund Advisors LP has sole voting power over 2,244,748 shares, sole dispositive power over 2,355,229 shares and shared voting and shared dispositive over 0 shares. |

(7) | Information was obtained from a Schedule 13G/A (Amendment No. 2) filed on February 8, 2019 with the SEC. The address for Private Capital Management, LLC is 8889 Pelican Bay Boulevard, Suite 500, Naples, Florida 34108. Private Capital Management, LLC has sole voting power and dispositive power over 609,538 shares and shared voting power and dispositive power over 1,668,924 shares. |

(8) | Includes shares of common stock issuable pursuant to 41,865 restricted stock units. |

(9) | Includes shares of common stock issuable pursuant to 15,783 restricted stock units. |

(10) | Includes shares of common stock issuable pursuant to 6,223 restricted stock units. |

(11) | Includes shares of common stock issuable pursuant to 4,668 restricted stock units. |

(12) | Includes shares of common stock issuable pursuant to 5,186 restricted stock units. |

(13) | The address of Mr. Cil and Mr. Dunnigan is 130 King Street West, Suite 300, P.O. Box 399, Toronto, ON M5X1E1, Canada. |

(14) | Includes 11,858 shares of our common stock held directly by Mr. Perelman and 7,364,413 shares of common stock held by Cambridge Holdings and 7,450,402 shares of our common stock issuable upon the conversion of the Series C Preferred Stock after giving effect to the removal of the Issuance Restriction. Mr. Perelman and Mr. Sloane control the managing member of Cambridge Holdings and therefore may be deemed to share voting and dispositive power of the shares held by Cambridge Holdings. The address for each of Mr. Perelman and Mr. Sloane is 853 Broadway, Suite 2014, New York, New York 10003. |

(15) | Includes 11,709 shares of our common stock held directly by Mr. Sloane and 7,364,413 shares of common stock held by Cambridge Holdings and 7,450,402 shares of our common stock issuable upon the conversion of the Series C Preferred Stock after giving effect to the removal of the Issuance Restriction. Mr. Perelman and Mr. Sloane control the managing member of Cambridge Holdings and therefore may be deemed to share voting and dispositive power of the shares held by Cambridge Holdings. The address for each of Mr. Perelman and Mr. Sloane is 853 Broadway, Suite 2014, New York, New York 10003. |

Equity Compensation Plans

The following table summarizes, as of December 30, 2018, the equity compensation plans under which our common stock may be issued to our directors, officers and employees. Our stockholders approved all plans.

Number of securities to be issued upon exercise of outstanding options, warrants and rights | Weighted-average exercise price of outstanding options, warrants and rights | Number of securities remaining available for future issuance under equity compensation plans | ||||||

Equity compensation plans approved by security holders | — | — | 3,664,567 | |||||

Equity compensation plans not approved by security holders | — | — | — | |||||

Total | — | — | 3,664,567 | |||||

19

CERTAIN RELATIONSHIPS AND RELATED TRANSACTIONS

Related Party Transaction Procedures

The board of directors has assigned responsibility for reviewing related party transactions to our audit committee. The board of directors and the audit committee have adopted a written policy pursuant to which certain transactions between us or our subsidiaries and any of our directors or executive officers must be submitted to the audit committee for consideration prior to the consummation of the transaction as required by the rules of the SEC. The audit committee reports to the board of directors on all related party transactions considered.

Series B Preferred Stock